Loans

Alexander Kelly is FA's Loan Specialist / point-of-contact for loans. We recommend that you speak to him and visit the Federal Student Loans - Types of Federal Student Loans website before borrowing a federal or private student loan. Mr. Kelly can be contacted by visiting the financial aid office in-person, emailing akelly15@gulfcoast.edu, or calling 850.872.3869.

In addition, GCSC has partnered with Student ConnectionsSM to help you understand your loan repayment commitments and address any issues you may encounter when the time comes to start paying back your loans. You can learn more about Student ConnectionsSM by visiting their Repay my Loans webpage.

Federal Direct Loans

Federal Direct Loans are financial aid funds that students or parents can borrow to pay for educational expenses. Federal Direct Loans have to be repaid with interest and require a FAFSA for the current academic year. Please visit the U.S. Department of Education's (ED) the Federal Student Aid - Default Management webpage to view GCSC's Cohort Default Rate and to see how it compares to other institutions / the national average. The percentage of students who borrow at GCSC can separately be found at ED's the U.S. Department of Education College Scorecard webpage.

- Subsidized loans are need-based, low interest, federally subsidized loans. These loans have no interest while the student is in school and attending at least six credit hours.

- Unsubsidized loans are not based on need and the interest is not subsidized by the federal government. Therefore, students are responsible for all interest accrued. More information can be found online at the Federal Student Aid - Direct Subsidized and Direct Unsubsidized Loans website.

- Origination Fee: An origination fee is a charge by the U.S. Department of Education for processing a federal student loan. The fee is a percentage of the total loan amount and is automatically deducted from the loan before it is disbursed to the school. This means the amount applied to the student’s account will be slightly less than the amount borrowed, though the student remains responsible for repaying the full loan amount, including the fee.

- Repayment doesn't begin until a student is no longer enrolled at least halftime.

- Students are given a one-time six month grace period to begin their repayment.

- Visit the Federal Student Aid - Calculate Your Federal Student Loan Repayment Options with Loan Simulator website for repayment estimator.

- Students are required to complete the Free Application for Federal Student Aid (FAFSA).

- Students applying for the Direct Stafford loan must be citizens or eligible non-citizens.

- Students must be enrolled in at least six credit hours (half-time) per semester. Please note that you will not receive a disbursement until you are actively attending the six credit hours.

- Students must meet all Satisfactory Academic Progress (SAP) standards and cannot exceed their aggregate or yearly loan limits, including loans received prior to attending GCSC.

- Loans will be processed for subsidized eligibility only, unless unsubsidized loans are specifically requested on the Direct Loan Request Form.

- Students have the ability to borrow less than the maximum student loan amount allowed per semester / year.

- All students must complete Exit Counseling when they graduate, withdraw, or drop below half-time enrollment status.

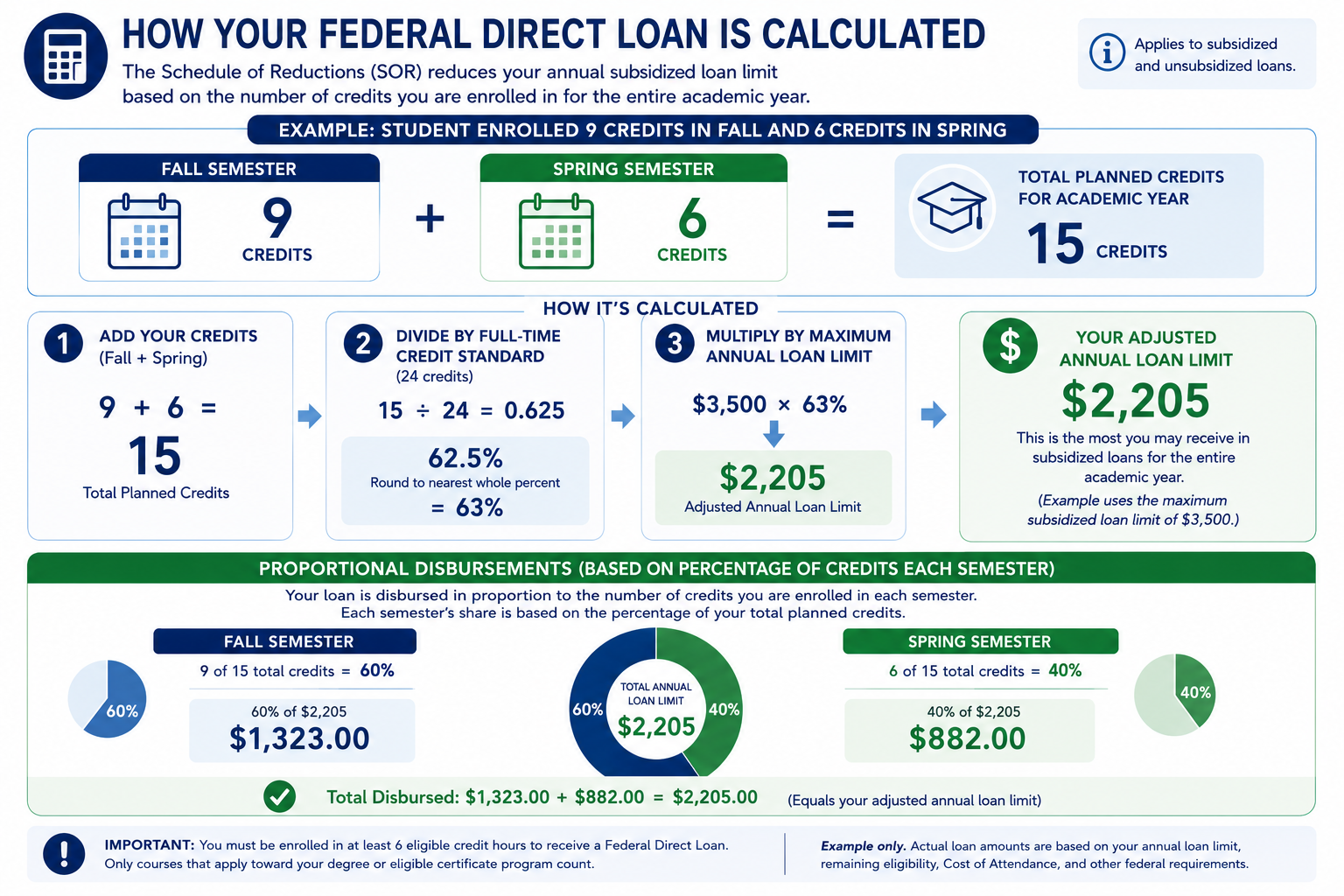

- Beginning with the 2026–2027 academic year, Federal Direct Loan annual loan limits are prorated based on the number of eligible credit hours in which a student is enrolled in for a current and future semester

- If you enroll in fewer than 12 eligible credit hours per semester, you will not qualify for the full annual Federal Direct Loan limit. Your maximum annual loan amount will be reduced based on your total eligible credit hours for the academic year using the federal Schedule of Reductions (SOR) formula.

- If your enrollment changes before or during the semester, your pending loan disbursement may be reduced or canceled if you no longer meet federal eligibility requirements.

- The infographic below provides an example of how the federal Schedule of Reductions (SOR) is used to calculate an adjusted annual Federal Direct Loan limit and proportional loan disbursements based on eligible credit hours. This example is provided for illustrative purposes only. Your actual loan eligibility and disbursement amounts may differ based on your individual circumstances, including your Cost of Attendance (COA), remaining financial need, annual loan limits, grade level, dependency status, and other federal eligibility requirements.

Students must complete the following steps to request a Federal Direct Loan (Subsidized or Unsubsidized):

- Complete a FAFSA by visiting the Federal Student Aid - Apply for Aid website

- Submit a 'Request a Federal Student Loan' form in My Student Dashboard

- Visit the Federal Student Aid website to complete –

- Returning students may also need to complete an "Annual Student Loan Acknowledgment" starting with the 2022-2023 academic year.

Once eligibility is determined, you will see award information on Student Dashboard --> Financial Aid--> Offer tab.

A "Notice of Guarantee and Disclosure Statement" indicating dollar amounts and disbursement dates for the terms requested will separately be mailed or emailed to you by ED within two weeks of your loan origination.

A Federal Direct Parent PLUS Loan is a credit-based low interest loan that a parent can borrow in order to fund their dependent child's education.

Parents must complete the following steps to request a Federal Direct Parent PLUS Loan:

- Visit the Federal Student Aid to –

- Submit a Parent PLUS pre-application

- Complete PLUS Entrance Counseling

- Complete a PLUS Master Promissory Note

- Complete an "Annual Student Loan Acknowledgment"

- Ensure that your student has completed a FAFSA by visiting Federal Student Aid - Apply for Aid website

- Submit a Federal Direct PLUS Loan Authorization Form to the financial aid office

Please note - all Federal Direct/Stafford Subsidized and Unsubsidized Loans will be awarded to the dependent student before Federal Direct PLUS loans.

Private / Alternative Loans

Private /alternative student loans are not funded or subsidized by the federal government; instead, they are funded by banks, credit unions, or other types of lenders. The bank or lender – not the federal government – sets interest rates, loan limits, terms, and conditions of private / alternative student loans. Please visit the Federal Student Loans - Types of Federal Student Loans website for more information.

- Research private / alternative loan lenders.

- Contact the private / alternative loan lenders that you're most comfortable with based upon your research in order to inquire about their application procedure.

- Once approved, complete and submit a Private Education Loan Self Certification Form to your private / alternative loan lender.

- Request private / alternative loan certification by emailing the Financial Aid Office at FA@GULFCOAST.EDU from your GCSC account.

Please note:

- GCSC uses Education Loan Management for all private / alternative loan certifications.

- Private / alternative loans will not be certified for continuing education courses, i.e. you have to be a degree or certificate-seeking student in order to receive private loan disbursement at GCSC.

What are the differences between federal DIRECT and private / ALTERNATIVE loans?

Federal student loans are loans made or guaranteed by the Department of Education. Private / alternative loans are any other type of student loans. While both federal student loans and private / alternative student loans allow you to borrow money to pay for education expenses, there are some distinct differences. Please visit the CFPB - What are the different ways to pay for college or graduate school? website for more information.

| Federal | Private / Alternative |

|---|---|

| You will not have to start repaying your federal student loans until you graduate, leave school, or change your enrollment status to less than half-time. | Many private student loans require payments while you are still in school. |

| The interest rate is fixed and is often lower than private loans and much lower than some credit card interest rates. View the current interest rates on federal student loans. | Private student loans can have variable interest rates, some greater than 18%. A variable rate may substantially increase the total amount you repay. |

| Undergraduate students with financial need will likely qualify for a subsidized loan where the government pays the interest while you are in school on at least a half-time basis. | Private student loans are not subsidized. No one will pay the interest on your loan other than you. |

| You don’t need to get a credit check for most federal student loans (except for PLUS loans). Federal student loans can help you establish a good credit record. | Private student loans may require an established credit record. The cost of a private student loan will depend on your credit score and other factors. |

| You won’t need a cosigner to get a federal student loan in most cases. | You may need a cosigner. |

| Interest may be tax deductible. | Interest may not be tax deductible. |

| Loans can be consolidated into a Direct Consolidation Loan. Visit the Federal Student Aid - Consolidating Student Loans website to learn about consolidation options. |

Private student loans cannot currently be consolidated into a Direct Consolidation Loan. |

| If you are having trouble repaying your loan, you may be able to temporarily postpone or lower your payments. | Private student loans may not offer forbearance or deferment options. |

| There are several repayment plans, including an option to tie your monthly payment to your income. | Private student loans may not offer forbearance or deferment options. |

| There is no prepayment penalty fee. | There may be prepayment penalty fees. |

| You may be eligible to have some portion of your loans forgiven if you work in public service. | It is unlikely that your lender will offer a loan forgiveness program. |

| Free help is available at 1-800-4-FED-AID and on our websites. | The Consumer Financial Protection Bureau's private student loan ombudsman may be able to assist you if you have concerns about your private student loan. |

Source: Student Aid.gov website